Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

First-Time Home Buyers • For Buyers • Infographics •

October 14, 2022

Tips for First-Time Homebuyers

For Sellers • FSBOs • Selling Myths •

September 29, 2022

If You’re Thinking of Selling Your House This Fall, Hire a Pro

If You’re Thinking of Selling Your House This Fall, Hire a Pro

Today’s market is at a turning point, making it more essential than ever to work with a real estate professional. Not only will a trusted real estate advisor keep you updated and help you make the best decisions based on current market trends, but they’re also experts in managing the many aspects of selling your house.

Here are five key reasons why working with a real estate professional makes sense today.

1. A Professional Follows the Latest Market Trends

With higher mortgage rates and moderating buyer demand, conditions are changing and staying on top of the latest market information is crucial when you sell.

Working with an expert real estate advisor helps ensure you can stay updated on what’s happening. They know your local area and follow national trends too. More importantly, they’ll know what this data means for you, and as the market shifts, they’ll be able to help you navigate it and make your best decision.

2. A Professional Helps Maximize Your Pool of Buyers

Your agent’s role in bringing in buyers is important. Real estate professionals have a large variety of tools at their disposal, such as social media followers, agency resources, and the Multiple Listing Service (MLS) to ensure your house is viewed by the most buyers. Investopedia explains why it’s risky to sell on your own without the network an agent provides:

“You don’t have relationships with clients, other agents, or a real estate agency to bring the largest pool of potential buyers to your home. A smaller pool of potential buyers means less demand for your property, which can translate into waiting longer to sell your home and possibly not getting as much money as your house is worth.”

3. A Professional Understands the Fine Print

Today, more disclosures and regulations are mandatory when selling a house. That means the number of legal documents you’ll need to juggle is growing. The National Association of Realtors (NAR) explains it best, saying:

“Selling a home typically requires a variety of forms, reports, disclosures, and other legal and financial documents. . . . Also, there’s a lot of jargon involved in a real estate transaction; you want to work with a professional who can speak the language.”

A real estate professional knows exactly what needs to happen, what all the fine print means, and how to work through it efficiently. They’ll help you review the documents and avoid any costly missteps that could occur if you try to handle them on your own.

4. A Professional Is a Trained Negotiator

If you sell without a professional, you’ll also be solely responsible for all the negotiations. That means you’ll have to coordinate with:

- The buyer, who wants the best deal possible

- The buyer’s agent, who will use their expertise to advocate for the buyer

- The inspection company, which works for the buyer and will almost always find concerns with the house

- The appraiser, who assesses the property’s value to protect the lender

In today’s changing market, buyers are regaining some negotiation power as bidding wars ease. Instead of going toe-to-toe with all the above parties alone, lean on an expert. They’ll know what levers to pull, how to address everyone’s concerns, and when you may want to get a second opinion.

5. A Professional Knows How To Set the Right Price for Your House

If you sell your house on your own, you may be more likely to overshoot your asking price. That could mean your house will sit on the market because you priced it too high for where the market is now. Today, pricing a house requires even more expertise to ensure you get it right. NAR explains it like this:

“A great real estate agent will look at your home with an unbiased eye, providing you with the information you need to enhance marketability and maximize price.”

Real estate professionals know the ins and outs of how to price your house accurately and competitively. To do so, they compare your house to recently sold homes in your area and factor in the current condition of your home. These steps are key to making sure it’s set to move quickly while still getting you the highest possible final sale price.

Bottom Line

Whether it’s following local and national trends and guiding you through a shifting market or pricing your house right, a real estate agent has essential insights you’ll want to rely on throughout the transaction. Don’t go at it alone. If you plan to sell your house, let’s connect.

First-Time Home Buyers • For Buyers • House Market Updates •

September 28, 2022

Why You Should Consider Condos as Part of Your Home Search

Why You Should Consider Condos as Part of Your Home Search

The historically low inventory over the past few years led to challenges for many buyers trying to find a home that met their needs and their budget. If you’re in the same boat, you should know the recent shift in the housing market may have opened up doors for you to restart your search.

The inventory of homes for sale has increased this year, and that’s giving buyers much needed options. As Danielle Hale, Chief Economist at realtor.com, says:

“. . . today’s shoppers have more than 5 homes to consider for every 4 they had at this time a year ago.”

But perspective is important. Overall, housing supply is still low. If you need even more choices, expanding your search by adding additional housing types, like condominiums, could help.

Exploring Condos Could Add Options That Fit Your Budget

One thing to consider is condos generally differ from single-family homes in average space and floorplans. But that size difference is one reason why condos can be a more affordable option. According to a recent report from realtor.com, condo buyers paid roughly 7% less for their home than buyers of other housing types last year. With rising mortgage rates and home prices, the relative affordability of a condo could be worth considering.

Remember, your first home doesn’t have to be your forever home. The important thing is to get your foot in the door as a homeowner. Buying a condo now can springboard you into a bigger home later on. An article from the Urban Institute explains:

“Because condos and co-ops are generally more affordable, they tend to help first-time homebuyers step onto the first rung of the homeownership ladder. These buyers often use the equity on their condo to then purchase a larger single-family home.”

In other words, owning a condo will help you start building wealth in the form of home equity. In time, the equity you build can fuel a future purchase should you decide you want to buy a home with more space or different amenities.

Condo Living Provides Several Great Perks

Boosting the number of options in your budget during your home search is just one reason to consider condos, but there are several other benefits to condo living.

First, they tend to require minimal upkeep and lower maintenance – and that can give you more time to spend doing the things you enjoy. A recent article from Bankrate highlights this, saying:

“Condos can be a good option for anyone who wants to keep home maintenance to a minimum . . . if the roof is leaking or the carpet in the lobby needs to be replaced, that’s not your responsibility — the condo association handles those duties.”

Plus, since many condos are located in or near city centers, they offer the added benefit of being in close proximity to work and leisure. Again, realtor.com explains:

“Buying a condo, which is generally less expensive than a single-family home, enables a household to afford to own in the middle of it all, and often means a newer-built home with less maintenance responsibility.”

Ultimately, owning and living in a condo can be a lifestyle choice. And if that appeals to you, they could give you the added options you need to buy your first home.

Bottom Line

Adding condominiums to your housing search could be a great move. If you’re ready to search condos in our area, let’s connect today.

For Sellers • House Market Updates • Selling Myths •

September 19, 2022

Will My House Still Sell in Today’s Market?

Will My House Still Sell in Today’s Market?

If recent headlines about the housing market cooling and buyer demand moderating have you worried you’ve missed your chance to sell, here’s what you need to know. Buyer demand hasn’t disappeared, it’s just eased from the peak intensity we saw over the past two years.

Buyer Demand Then and Now

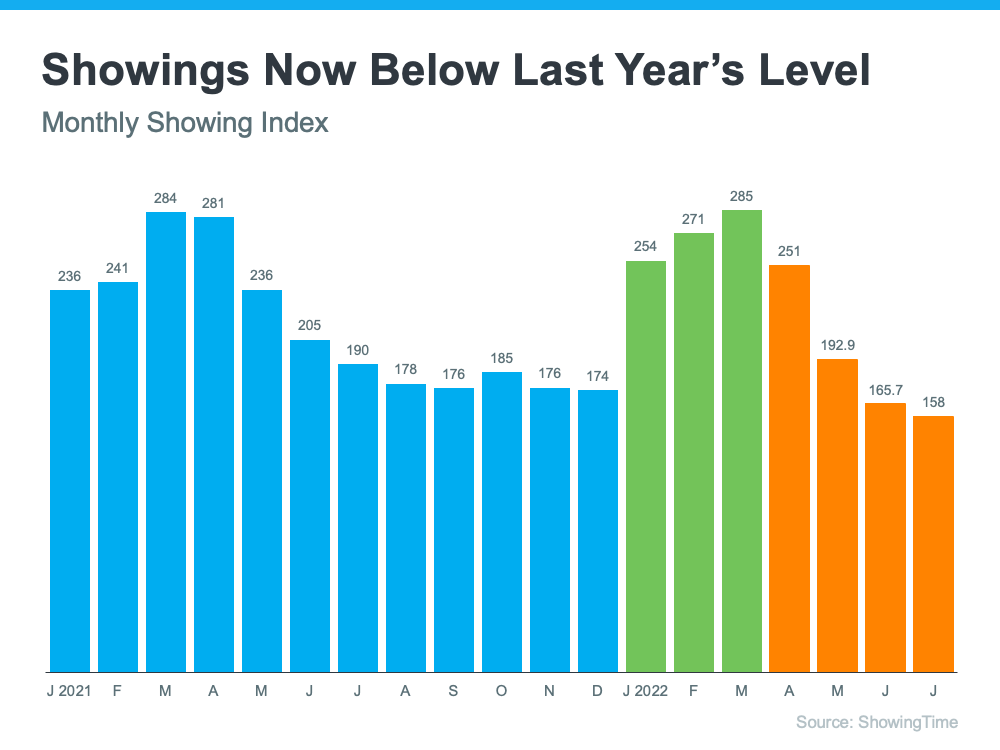

During the pandemic, mortgage rates hit record lows, and that spurred a significant rise in buyer demand. This year, as rates increased due to factors like rising inflation, buyer demand pulled back or softened as a result. The latest data from ShowingTime confirms this trend (see graph below):

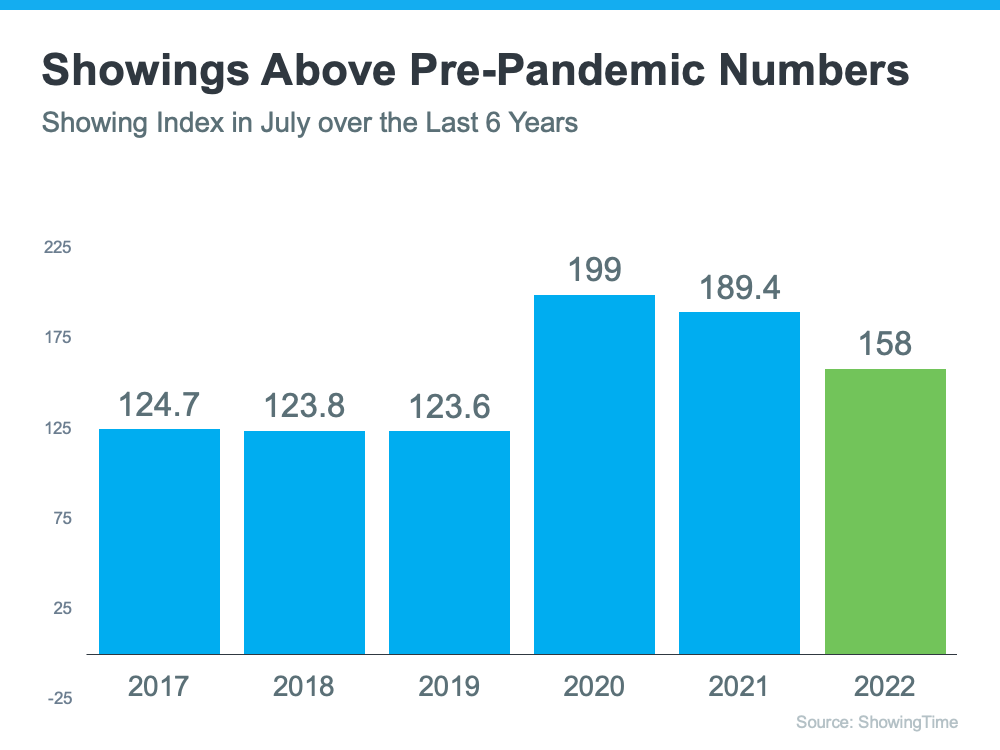

The orange bars in the graph above represent the last few months of data and the clear cooldown in the volume of home showings the market has seen since mortgage rates started to rise. But context is important. To get the full picture of where today’s demand stands, let’s look at the July data for the past six years (see graph below):

This second visual makes it clear that, while moderating compared to the frenzy in 2020 and 2021, showing activity is still beating pre-pandemic levels – and those pre-pandemic years were great years for the housing market. That goes to show there’s still demand if you sell your house today.

What That Means for You When You Sell

The key to selling in a changing market is understanding where the housing market is now. It’s not the same market we had last year or even earlier this year, but that doesn’t mean the opportunity to sell has passed.

While things have cooled a bit, it’s still a sellers’ market. If you work with a trusted local expert to price your house at the current market value, the demand is still there, and it should sell quickly. According to a recent survey from realtor.com, 92% of homeowners who sold in August reported being satisfied with the outcome of their sale.

Bottom Line

Buyer demand hasn’t disappeared, it’s just moderated this year. If you’re ready to sell your house today, let’s connect so you have expert insights on how the market has shifted and how to plan accordingly for your sale.

First-Time Home Buyers • For Buyers • House Market Updates • Move Up Buyers •

September 15, 2022

Buyers Are Regaining Some of Their Negotiation Power in Today’s Housing Market

Buyers Are Regaining Some of Their Negotiation Power in Today’s Housing Market

If you’re considering buying a home today, there’s welcome news. Even though it’s still a sellers’ market, it’s a more moderate sellers’ market than last year. And the days of feeling like you may need to waive contingencies or pay drastically over the asking price to consider your offer may be coming to a close.

Today, you should have less competition and more negotiating power as a buyer. That’s because the intensity of buyer demand and bidding wars is easing this year. So, if bidding wars were the biggest factor that had you sitting on the sidelines, here are two trends that may be just what you need to re-enter the market.

1. The Return of Contingencies

Over the last two years, more buyers have been willing to skip important steps in the home buying process, like the appraisal or inspection, to try to win a bidding war. But now, fewer people are waiving the inspection and appraisal.

The latest data from the National Association of Realtors (NAR) shows the percentage of buyers waiving their home inspection and appraisal is declining. And a recent survey from realtor.com confirms more sellers are accepting offers that include these conditions today. According to their August study:

- 95% of sellers reported buyers requested a home inspection

- 67% of sellers negotiated with buyers on repairs as a result of the inspection findings

This shows buyers are more able to include these conditions in their offers today and negotiate as needed based on the inspection outcome.

2. Sellers Are More Willing To Help with Closing Costs

Generally, closing costs range between 2% and 5% of the purchase price for the home. Before the pandemic, sellers used a common negotiation tactic to cover some of the buyer’s closing costs to sweeten the deal. This didn’t happen much during the peak buyer frenzy over the past two years.

Today, as the market shifts and demand slows, data from realtor.com suggests this is making a comeback. A recent article shows 32% of sellers paid some or all of their buyer’s closing costs. This may be a negotiation tool you’ll see as you purchase a home. Remember that limits on closing cost credits are set by your lender and can vary by state and loan type. Work closely with your loan advisor to understand how much a seller can contribute to closing costs in your area.

Bottom Line

Regardless of the extremely competitive housing market of the past several years, today’s data suggests negotiations are starting to come back on the table. This is good news if you’re planning to enter the housing market. Let’s connect to find out how the market is shifting in our area.

For Buyers • For Sellers • House Market Updates •

September 14, 2022

Is the Real Estate Market Slowing, or Is This a Housing Bubble?

Is the Real Estate Market Slowing, or Is This a Housing Bubble?

The talk of a housing bubble in the coming year seems to be at a fever pitch as rising mortgage rates continue to slow down an overheated real estate market. Over the past two years, home prices have appreciated at an unsustainable pace causing many to ask: are things just slowing down, or is a crash coming?

To answer this question, there are two things we want to understand. The first is the reality of the shift in today’s housing market. And the second is what experts say about home prices in the coming year.

The Reality of the Shift in Today’s Housing Market

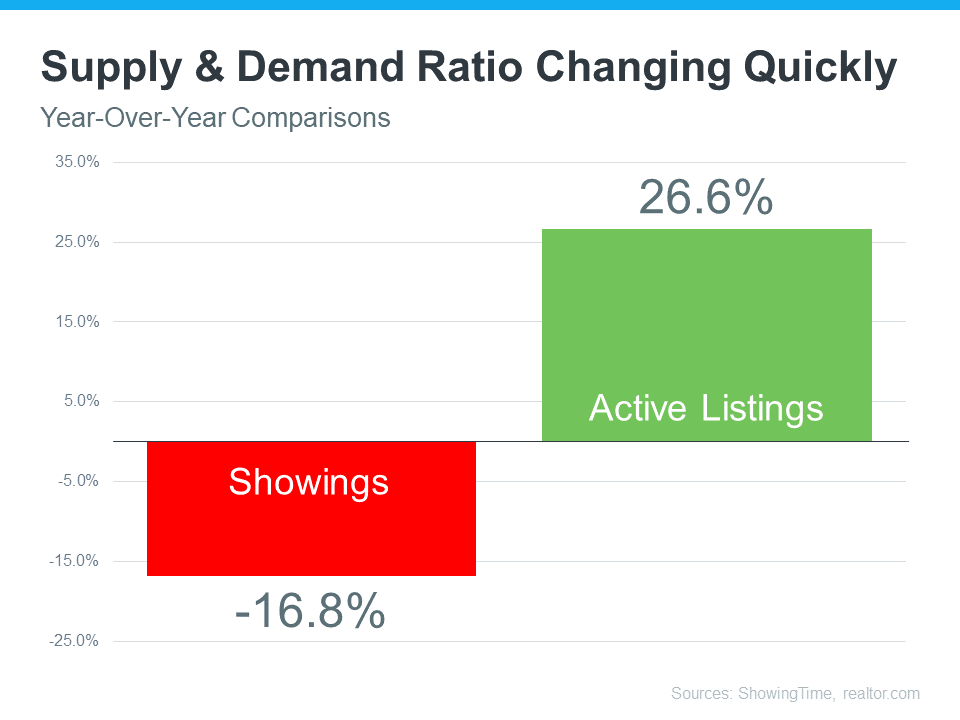

The reality is we see an inflection point in housing supply and demand. According to realtor.com, active listings have increased more than 26% over last year, while showings from the latest ShowingTime Showing Index have decreased almost 17% from last year (see graph below). This is an inflection point for housing because, over the past two years, we’ve seen massive demand (showings) and not enough homes available for sale for the number of people that wanted to buy. That caused the market frenzy.

Today, supply and demand look very different, and the market is slowing down from the pace we’ve seen. This offers proof of the sudden slowdown so many people are feeling.

What Experts Are Saying About Home Prices in the Coming Year

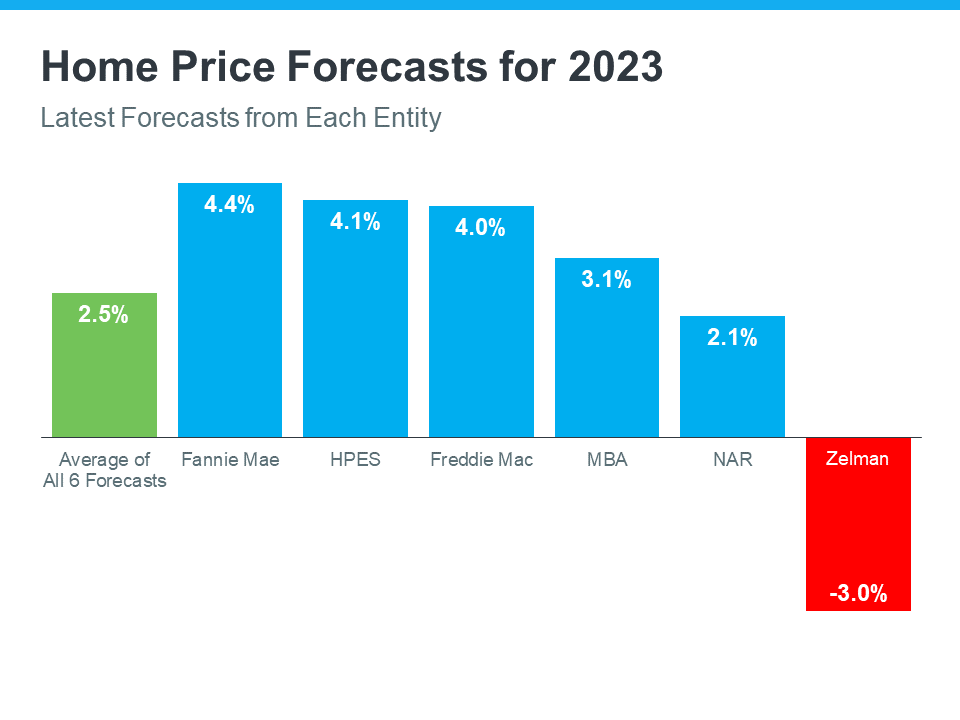

Most experts forecast home price appreciation in 2023, but at a much slower pace than the last two years. The average of the six forecasters below is for national home prices to appreciate by 2.5% in the coming year. Only one of the six is calling for home price depreciation.

When we look at the shift and what experts say, we can conclude the national real estate market is slowing down but is not a bubble getting ready to burst. This isn’t to say that a few overheated markets won’t experience home price depreciation, but there isn’t a case to be made for a national housing bubble.

Bottom Line

The real estate market is slowing down, causing many to fear we’re in a housing bubble. What we’ve experienced in the housing market over the past two years were historic levels of demand and constrained supply. That led to homes going up in value at a record pace. While some overheated markets may experience price depreciation in the short term, according to experts, the national real estate market will appreciate in the coming year.

First-Time Home Buyers • For Buyers • House Market Updates • Move Up Buyers •

September 13, 2022

Three Things Buyers Can Do in Today’s Housing Market

Three Things Buyers Can Do in Today’s Housing Market

It’s clear the 2022 housing market has been defined by rising mortgage rates. With rates on the rise, it’s also become more costly to purchase a home. According to the National Association of Realtors (NAR):

“Compared to one year ago, the monthly mortgage payment rose to $1,944 from $1,265, an increase of 53.7%.”

If you’re thinking of buying a home or have been trying to recently, that’s a big increase in a monthly mortgage payment – and it may be causing you to press pause on your plans. This jump is making homes less affordable, especially compared to the last two years when mortgage rates were at historic lows.

The good news is you can navigate today’s housing market and this rising rate environment with a few simple tips. Here are three things you may want to consider to help make your homeownership goals a reality.

1. Expand Your Search Area and Criteria

If you’ve been looking for a home in the city center or a specific area that’s starting to feel out of your price range, you may want to try looking a little further out in a location that could be more affordable. Expanding your search location or re-prioritizing the items on your wish list can open up opportunities you haven’t considered, and that could help you afford more of what you need (and want) in a home. As CNET notes:

“Area growth is likely to keep pace with the market, which means that the outskirts of town might be hopping within five years. Consider stepping out of your ideal location by searching in the nearby cities. You may find better prices and more square footage.”

2. Explore Alternative Financing Options

Working with a trusted lender to learn about the different loan types and options is essential too. According to Nerd Wallet:

“A variety of mortgages are available with varying down payment and eligibility requirements.”

Experts know how to point you in the right direction when it comes to exploring ways to find the best home loan for your situation. With rising mortgage rates making it more costly to finance a home today, there may be an ideal option out there your loan officer can introduce you to. This could make a home purchase more affordable and within your financial reach over the life of your loan.

3. Look for Grants, Gift Funds, and Down Payment Assistance

There are also many options available when it comes to securing the funding you need to purchase a home. One valuable resource to explore is downpaymentresource.com. Searching for specific down payment assistance options available in your local community could be a game changer when it comes to taking your first step toward homeownership. As NAR indicates:

“Many local governments and non-profit organizations offer down-payment assistance grants and loans, targeted to area borrowers and often with specific borrower requirements.”

Plus, there are programs and special benefits for individuals working in certain professions or with unique statuses, including teachers, doctors and nurses, and veterans.

Ultimately, that means there are many federal, state, and local programs available for you to explore. The best way to do that is to connect with a local real estate professional and your lender to learn more about what’s available in your area.

Bottom Line

If you’ve been searching for a home and have found yourself stepping out of the process because you’re worried about rising costs, let’s connect. Having a team of local advisors on your side may be just what you need to guide your search in a new and more affordable direction.

For Buyers • For Sellers • House Market Updates • Infographics •

August 26, 2022

What Does a Recession Mean for the Housing Market? [INFOGRAPHIC]

![What Does a Recession Mean for the Housing Market? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/08/25120040/20220826-MEM-1046x2165.png)

Baby Boomers • Demographics • For Sellers • Senior Market •

August 18, 2022

Planning To Retire? Your Equity Can Help You Reach Your Goal.

Planning To Retire? Your Equity Can Help You Reach Your Goal.

Whether you’ve just retired or you’re thinking about retirement, you may be considering your options and trying to picture a whole new stage of your life. And you’re not alone. Research from the Retirement Industry Trust Association (RITA) shows 10,000 Baby Boomers reach the typical retirement age (65) every day, and only 47% of the people in that generation have already retired.

If this sounds like you, one thing worth considering is whether or not your current home will suit your new lifestyle. If your home doesn’t have the features or benefits you’re looking for, the good news is, you may be in a better position to move than you realize.

That’s because, if you already own a home, you’ve likely built-up significant equity, and that can help you fuel your next move. According to the National Association of Realtors (NAR):

“A homeowner who purchased a typical home five years ago would have gained $125,300 from just price appreciation alone.”

In fact, over the last twelve months, CoreLogic reports the average homeowner in the United States gained roughly $64,000 in equity due to home price appreciation.

You can use your equity to help you achieve your homeownership goals. Whether you want to downsize, move closer to loved ones, or buy a home in a dream destination, your equity can help get you there. It may be some (if not all) of what you’d need as your down payment on a home that better fits your changing needs.

To find out how much equity to have in your home, reach out to a trusted real estate professional today.

Bottom Line

Retirement is a big step and so is buying or selling a home. As you move into this new phase of life, let’s connect so you have an expert to guide you through the process as you sell your current home and give you expert advice as you buy one that’ll better suit your needs.

For Buyers • For Sellers • House Market Updates • Interest Rates • Pricing •

August 16, 2022

What Would a Recession Mean for the Housing Market?

What Would a Recession Mean for the Housing Market?

According to a recent survey from the Wall Street Journal, the percentage of economists who believe we’ll see a recession in the next 12 months is growing. When surveyed in July 2021, only 12% of economists consulted thought there’d be a recession by now. But this July, when polled, 49% believe we will see a recession in the coming 12 months.

And as more recession talk fills the air, one concern many people have is: should I delay my homeownership plans if there’s a recession?

Here’s a look at historical data to show what happened in real estate during previous recessions to help prove why you shouldn’t be afraid of what a recession would mean for the housing market today.

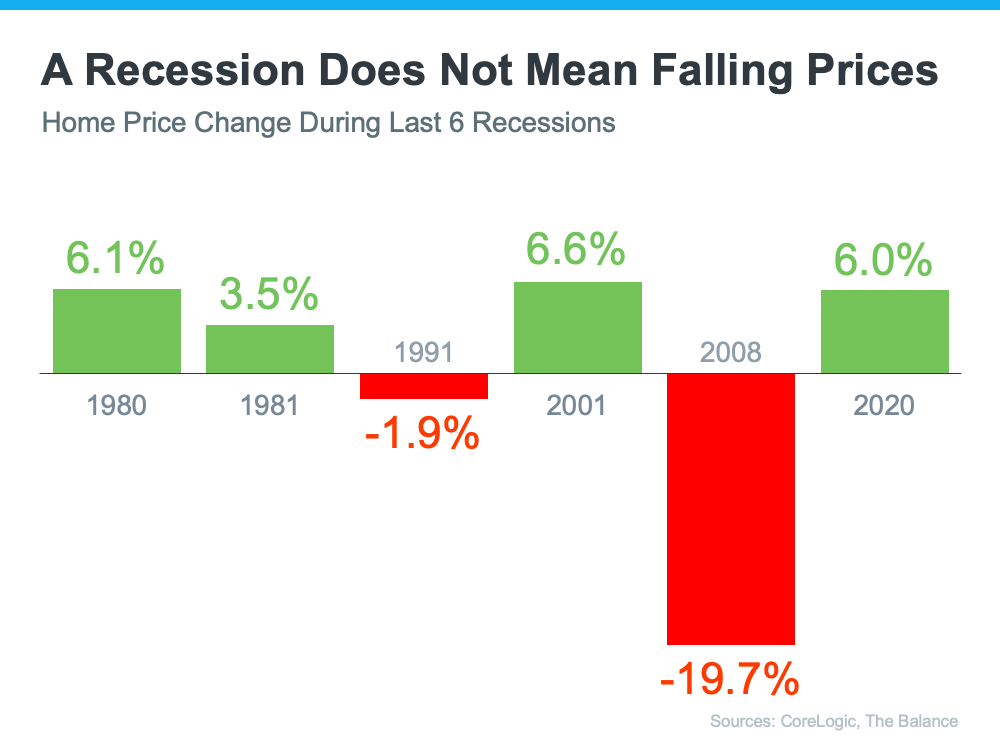

A Recession Doesn’t Mean Falling Home Prices

To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at the recessions going all the way back to 1980, home prices appreciated in four of the last six recessions. So, historically, when the economy slows down, it doesn’t mean home values will fall.

Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession would repeat what happened then. But this housing market isn’t about to crash. The fundamentals are very different today than they were in 2008. So, don’t assume we’re heading down the same path.

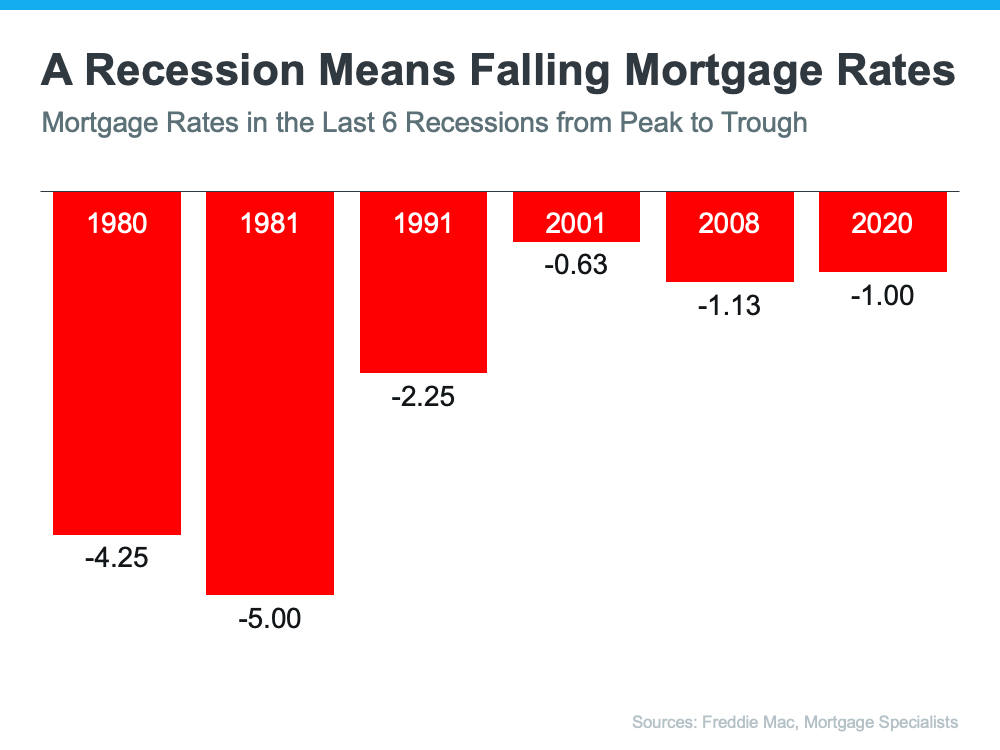

A Recession Means Falling Mortgage Rates

Research also helps paint the picture of how a recession could impact the cost of financing a home. As the chart below shows, historically, each time the economy slowed down, mortgage rates decreased.

Fortune explains that mortgage rates typically fall during an economic slowdown:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

And while history doesn’t always repeat itself, we can learn from and find comfort in the historical data.

Bottom Line

There’s no doubt everyone remembers what happened in the housing market in 2008. But you don’t need to fear the word recession if you’re planning to buy or sell a home. According to historical data, in most recessions, home price gains have stayed strong, and mortgage rates have declined.

If you’re thinking about buying or selling a home, let’s connect so you have expert advice on what’s happening in the housing market and what that means for your homeownership goals.